Our latest news and analysis.

Managing An Unsolicited Acquisition Approach

Everyone who starts a company shares dreams of an unsolicited acquisition approach: that one day they are going to get a knock on the door and standing there will be a smiling Sergei Brin and Larry Page from Google with a giant cheque in their hands.

And you, the company founder, are going to look them square in the eye and greet them with the words, “what took you so long?”

Now, it may not necessarily be the multi-billionaire founders of Google who will end up knocking on your door, but it is certainly not uncommon for a business owner to receive an unsolicited acquisition approach to buy their business.

In our experience, receiving such offers can be the beginning of either a highly positive or negative experience. Following the process through takes significant time and there are no guarantees that an initial approach will result in an offer, let alone a completed transaction.

In this post, we will look at some of the things you can do to effectively deal with an unsolicited acquisition approach that will result in the minimum amount of disruption to the day-to-day running of your business and your life.

Key steps to dealing with an unsolicited acquisition approach:

Step One: Know why you’re in business

The first step to effectively managing an unsolicited acquisition approach is to understand exactly why you are in business. Of course, everyone is in business to make money but on a deeper level, people’s motivations vary.

Particularly in the start-up world, for example, everyone that starts a business does so to achieve that fabled exit. From the very beginnings of a start-up’s life, the company’s founders and the investors who back them are driving hard for a sale.

As a result, there is little doubt that they will at the very least hear out most unsolicited offers.

However, there are many people in business who have very different motivations. There are countless owners, for example, who are running a company with the view to eventually passing it on to their children.

There are other people running businesses who decided to go out on their own to escape corporate life and have absolutely no desire to ever work for “the man” again. Others simply love what they do and want to keep working until they are carried out in a box.

The bottom line is that the first step to dealing with an unsolicited acquisition approach is to really understand why you are in business. It will determine whether you have any interest at all in engaging with an unsolicited knock on the door. You don’t want to be three months into the process only to say to yourself, “You know what, I actually don’t want to sell.”

If you are interested, then be interested. If you are not, be polite yet direct and close the conversation down before it starts. So long as you’re not rude, everyone appreciates not wasting their time.

Step Two: Consider if now is the time

As an extension to Step One, even if you are theoretically open to selling your business, it is also important to think through whether ‘now’ is the right time to be considering an unsolicited acquisition approach.

It may be that you have a clear growth strategy that you are only part the way through and that you are confident that the company will be worth a lot more in 18 or 24-months’ time. If that’s the case, then ‘now’ may not be the time.

Alternatively, it may be that your industry is going through a cyclical downturn that is making the going tough for everybody. If your business remains viable and you have seen the same cycle repeat itself before, you may decide that you don’t want to talk to apparent bottom feeders.

You often see this phenomenon with public companies. A business might be finding things tough going because of a general downturn in the industry or be experiencing some operational problems and suddenly along comes a suitor offering to pick up the company on the cheap.

There is nothing wrong with a potential buyer giving it a go but unlike listed companies that have a fiduciary duty to shareholders to generally at least listen to unsolicited acquisition approaches, as a private company, there are no such obligations.

So, be clear in your own mind whether ‘now’ is the time to be engaging. If it’s not, offer a polite ‘not now’ and move on.

Step Three: Listen carefully to the unsolicited acquisition approach

If you decide to engage, you should listen carefully to what the prospective acquirer has to say without pre-judgement. You may well be talking to someone who is about to hand you a significant amount of money. Being cagey to the point of being rude or obtuse is pointless and unproductive.

At the same time, you should feel absolutely no pressure to indicate whether you are interested in their proposal and you should certainly resist the temptation to disclose any meaningful information about your business at this point.

Remember, they approached you. So, they should be the ones doing the early talking and it is on them to convince you that it’s a conversation worth pursuing.

Step Four: Understand exactly what they are looking for

Having listened to the potential acquirer’s broad pitch, the next immediate step is to determine whether it is worth investing any further time in the exercise. There are two broad aspects to making that decision.

First, you need to clearly understand exactly what the prospective acquirer is looking for and whether your company, prima facie, meets their criteria. Typically, that will revolve around minimum financial metrics such as revenue or earnings.

For example, the purchaser might say that their board has set a requirement that any acquisition must have an EBITDA of, say, at least $5m. If your company has an EBITDA of only $2m, then it is probably not worth spending more time on the conversation.

If the person knocking on your door is vague in terms of what they are looking for and what their purchase criteria are, in our view, that is a warning sign that suggests they are more tyre kickers than serious buyers.

Second, you need to understand how the potential acquirer will value your business, whether their approach is consistent with yours and if it will ultimately satisfy your valuation expectations and also you need to understand their broad approach to deal structuring.

For example, if the acquirer says that they tend to value businesses at 2.0-3.0X’s EBIT and that would value your business at, say, $8m but you believe that on an asset basis your company is worth at least $15m, that gap is unlikely to be reconciled to the satisfaction of both parties.

It is also important to understand how they typically structure deals. Perhaps their standard approach is to insist on a three-year earn-out arrangement or to impose a minimum acquisition stake.

Understanding these fundamental aspects of the prospective acquirer’s thinking and approach to doing the deal can save you from wasting time on a transaction that will never meet your needs and expectations.

Step Five: Undertake your own preliminary due diligence.

If you decide that your business is in the ballpark of what the other party is looking for and that their views on value and deal structure seem reasonable, you then need to decide whether as a counter-party, they can do the deal. You don’t want to continue down the path if they can’t.

Sometimes the answer to this question is obvious.

For example, if the counter-party is a significantly larger listed entity with a long track record of doing deals in your industry, then the risk that they will be unlikely to complete a transaction would appear to be relatively low.

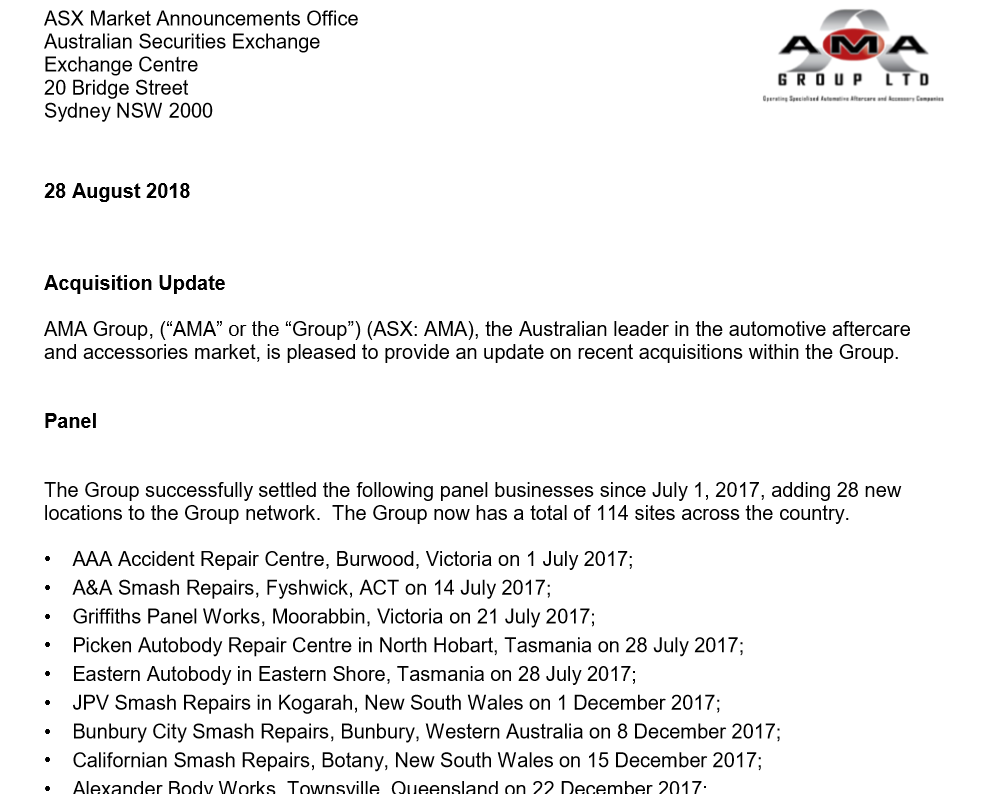

Below is a screen grab from an ASX update from the listed smash repair company AMA Group Limited, that lists the 28 panel beating companies the company acquired between July 1, 2017, and August 28, 2018.

Based on the above, any panel beating business receiving an unsolicited approach from AMA could proceed with reasonable confidence that as a counter-party, the risk of them failing to complete a transaction in relatively low.

The same could be said if you were approached by an established private equity firm with a track record of completing acquisitions within your industry. Again, it is more than likely that they would be able to complete.

For a detailed overview of what private equity looks for in acquisition opportunities, please click here.

The reality is that you might be approached by a party that is not a large, listed industry player or a well-known private equity firm. In such a case, you need to decide whether the party is a genuine and capable prospective purchaser. This is ultimately a judgement call.

To help you answer the question, you can conduct desktop research into the company, ask them direct questions about their financial capacity and acquisition history and so on. You might even ask trusted industry associates whether they have any insight to offer.

Step Six: What to do if you decide to engage

If you decide based on the above process that you want to engage further, your next immediate step is to take control of the process. The starting point for doing so is by having a carefully considered confidentiality plan in place to protect your proprietary information.

Start by putting in place a carefully drafted confidentiality agreement (“CA”) that sets out your respective rights and obligations in terms of dealing with your confidential information.

In addition to implementing a CA, it is important to determine what information you are prepared to disclose and when. Just because you have a CA in place does not mean that you suddenly divulge every fact and figure about your company.

Information should be released in a staged manner with you disclosing just enough information at each stage to firm up the counter-party’s interest in putting forward a formal proposal. Part of this process is also deciding on what you will not disclose until you have a formal, written offer in place.

As you are engaging with the unsolicited approach, another important consideration is whether to reach out to other prospective acquirers and to run a formal sale process.

Running a formal process has the potential benefit of driving competitive tension for your business, which should result in a higher price. At the same time, it is also a less discrete and more involved, and time-consuming exercise.

The key point is that you want to decide whether to launch a formal sale process on your own terms and not to be rushed by the other party. If your discussions rapidly evolve, they could be seeking exclusivity before you have thought deeply about the issue.

This is a strategic decision that is best made with appropriate corporate advice.

Unsolicited acquisition approaches are not uncommon and require careful thought to maximise the opportunities and minimise the risks involved. If you would like to have a confidential discussion about how CFSG can assist you in successfully completing the sale of your business, please contact us.